WHAT IS AN EXAMPLE OF A 1031 EXCHANGE?

Meridian has a track record of helping investors identify, analyze and close successfully on 1031 exchange properties which offer:- Stable Returns in Quality Neighborhoods

- Turnkey Investments with Affordable Entry Prices

- Easy Due Diligence with Fast, Non-Competitive Closings

- Professional In-House Property Management

- Capital Reallocation for Increased Investor ROI

- Cash & Mortgage Boot Solutions

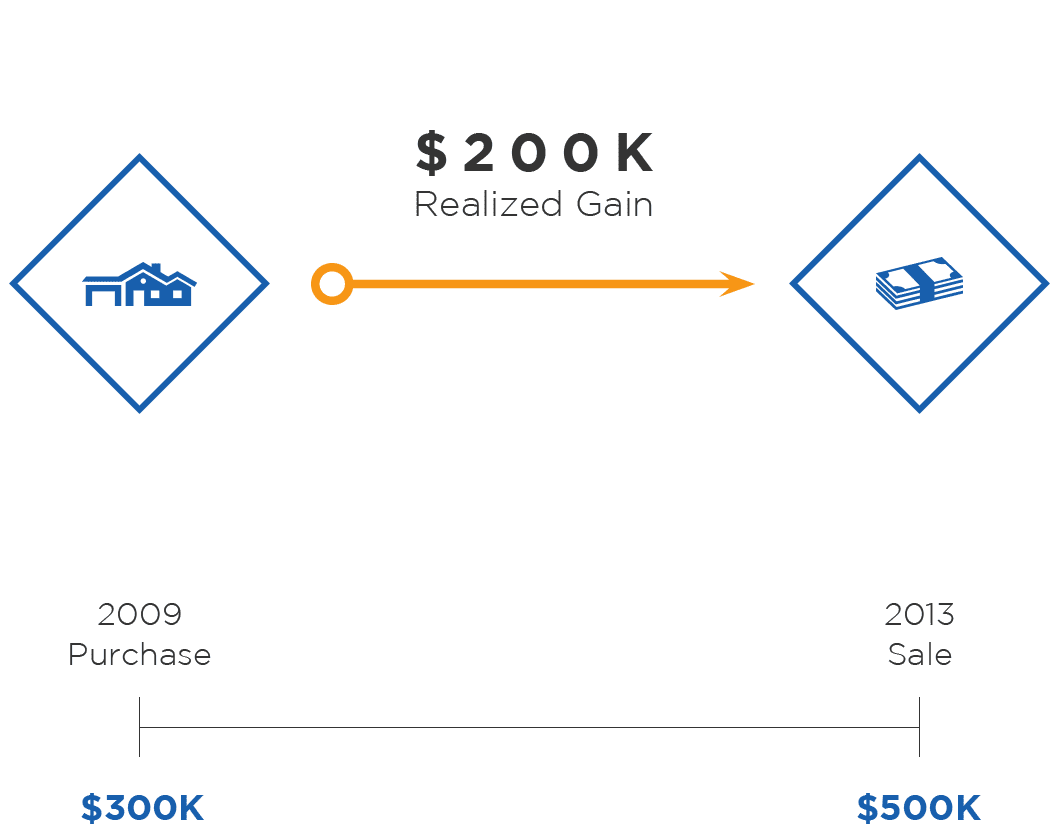

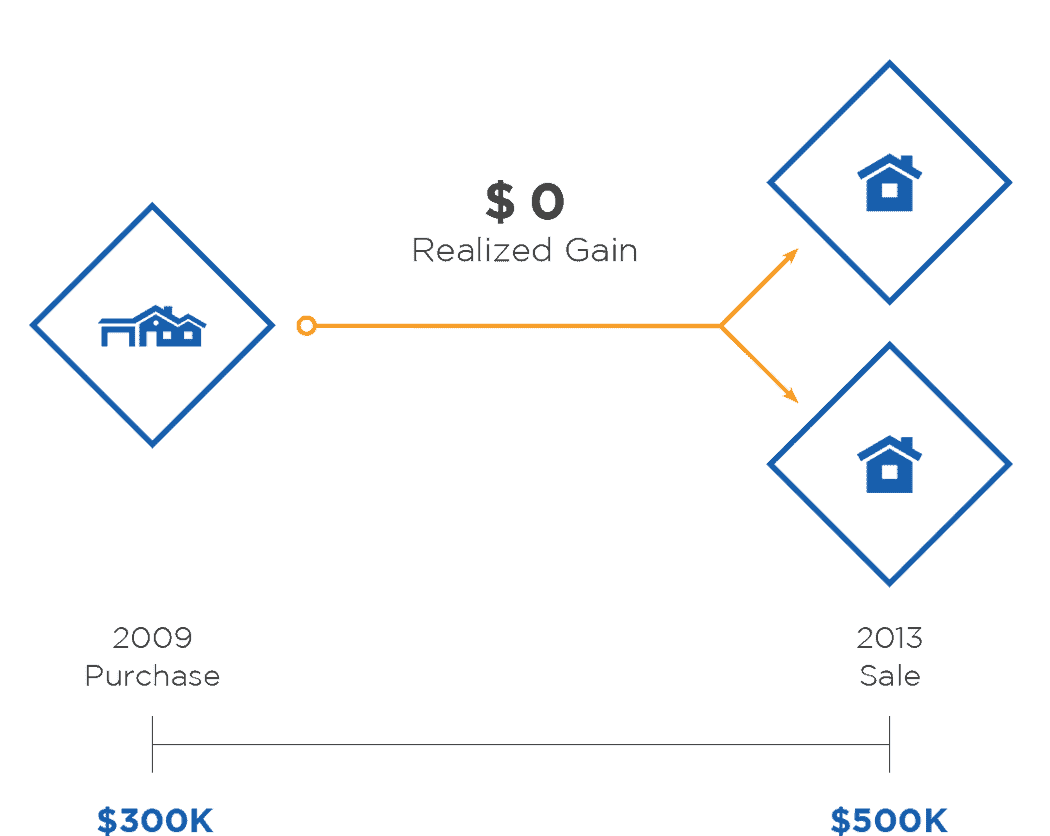

RESIDENTIAL 1031 EXCHANGE EXAMPLE

Property Management Can Make or Break a Real Estate Investment

Before you sign a management agreement, make sure your property management company excels in

Understanding 1031 Exchanges and Property Requirements

A 1031 exchange, or the like-kind or tax-deferred exchange, is a real estate transaction

How to Decide if a 1031 Exchange is Right for You

A 1031 exchange is the act of making a likekind trade of two assets

1031 Exchange Basics

What is a 1031 Exchange? When an investor sells investment real estate for a

4 Tax Benefits of a 1031 Real Estate Exchange

There are significant tax benefits when you take advantage of a 1031 taxdeferred real

History of the 1031 Exchange Program

What is a 1031 Exchange? A 1031 exchange is a tax strategy under Section

5 Little Known Facts that Could Affect Your 1031 Tax Deferment

A 1031 tax-deferred exchange involves trading two inkind properties. The two properties do not

A 7 Step Guide to Choosing Your 1031 Exchange Service

Real estate investors seeking to preserve the value of their assets, may find a